Do you understand the financial documents that govern your day-to-day life?

They may not be meeting federal plain-language guidelines

Regulations for the financial industry in Canada

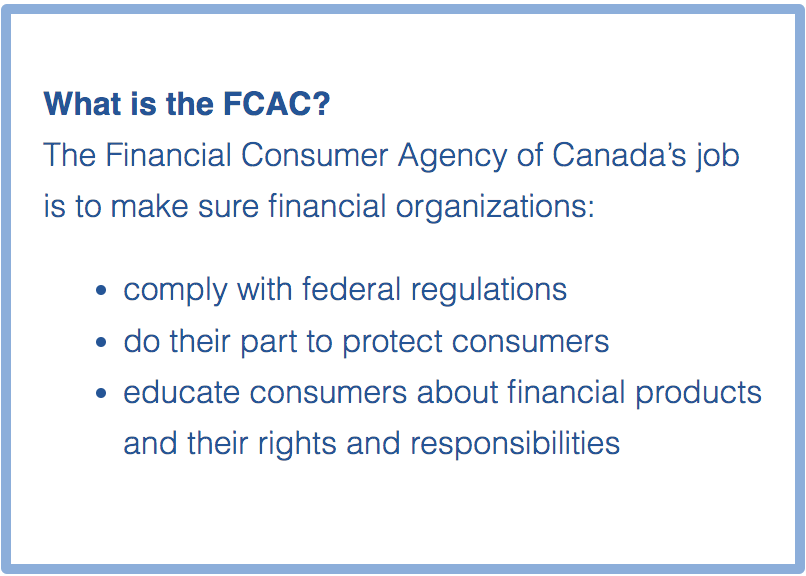

The Cost of Borrowing Regulations require federally regulated financial institutions to create disclosure documents for consumers that are clear, simple, and not misleading. The Financial Consumer Agency of Canada (FCAC) wrote guidance to help financial institutions meet new legislation and regulations. Banks and other organizations must apply the following five clear language principles to their writing:

Know your audience.

Make your material understandable by planning your text.

Write clearly.

Use the visual presentation to enhance your text.

Test your material.

How well are these principles being applied?

There is a growing movement towards plain language in the financial industry, and that’s good progress. Wordsmith works with many clients—both regulators and financial firms—to help them meet the FCAC guidance. But it is also clear there’s more to be done.

The official answer

FCAC reviewed the policies and procedures of federally regulated financial institutions to see how many were actually applying the clear language guidance. Their review concluded that while some were implementing the principles effectively, “many FRFIs [federally regulated financial institutions] made minimal efforts.”

Our recent experience

Here’s a pretty great example of an agreement that clearly doesn’t meet FCAC’s guidance. It’s a loan agreement that one of us signed last month for a small-ish purchase of a camper. It’s the sort of thing one might be tempted to use to start a campfire.

Security and Title: You give us a security interest in your vehicle (including any attachments, accessions, repairs, or replacement parts or other equipment placed on your vehicle) together with all proceeds (which includes insurance proceeds) from such goods to secure the repayment of the Loan (and the payment of all other amounts you may owe us under any other agreement from time to time). We also retain title to your vehicle until you repay your Loan and any other debts you owe us. When you repay your Loan and any other debts you owe us we will discharge our security interest in your vehicle and title to your vehicle will then transfer to you. We may register a financing statement to perfect our security interest in your vehicle and, if permitted by law, you waive your right to receive a copy of any financing statement or financing change statement that we register.

Our before-and-after examples of FCAC compliance

We thought you might find it interesting to read some examples of financial documents written in plain language. These are from work we did to help banks comply with the FCAC guidelines. Let us know what you think.

Example #1 Revised

You are liable for unauthorized use of your Card if you do not:

notify the bank in accordance with section 7 of this Agreement

keep your PIN confidential as section 6 of this Agreement requires

cooperate with the bank when it investigates the unauthorized use

If one of these situations applies, we limit your liability to your daily withdrawal limit.

Example #1 Before

You are not liable for any unauthorized use of your Card except in the following circumstances in which case your liability each day is limited to your Daily Withdrawal Limit:

in the event that you fail to notify the bank in accordance with section 7 of this Agreement;

in the event that you fail to keep your PIN confidential in accordance with section 6 of this Agreement; or

in the event that you fail to cooperate with the bank in its investigation of the unauthorized use

Example #2 Revised

You must update this loan information later if we ask you to do so.

Example #2 Before

The Borrower will supply such further information as the Bank may require from time to time to make current the information set out in the loan application (the "Application").

Example #3 Revised

Should a GIC be used to fund a payment or withdrawal from your primary plan or your Education Savings Plan, the portion redeemed will reduce the Principal investment, as referred to below, and no interest shall be payable on the redeemed amount.

Example #3 Before

Should a GIC be used to fund a payment or withdrawal from your primary plan or your Education Savings Plan, the portion redeemed will reduce the Principal investment, as referred to below, and no interest shall be payable on the redeemed amount.

Example #4 Revised

The amount you can recover can’t be more than what you paid.

Example #4 Before

Recovery hereunder by the debtor shall not exceed amounts paid by the debtor hereunder.

Decide for yourself

We encourage you to peek at your own financial documents—whether they’re credit card agreements, banking or mortgage documents, or investments. Do they meet the five principles above? If they don’t, you can let your financial institution know they could (and need to) go further.